Julia's Blog

Julia's Blog

I am not objecting to the replacement of the 50% discount with indexation. Sometimes indexation will produce a lesser capital gain than the 50% discount as under the discount half of your gain would be taxable no matter how bad inflation had been. With indexation at least you are only taxed on the true gain. It is just a so much more complicated calculation. When the 50% discount was introduced inflation was high, it was a reasonable average but most of all it just simplified things. In return for the 50% discount not only was indexing for inflation given up but also averaging out the tax rate on the gain by dividing the gain by 5 and adding that to your taxable income, looking at the average tax rate on that 1/5th and applying that to the other 4/5ths. The new regime ignores the fact that the gain has been made over many years, so should not artificially increase your income in one year. It goes even further to attack low gains and low income earners by setting a minimum tax rate of 30%. The minimum tax rate only hurts the low income taxpayers not the wealthy. On a taxable income of $227,000 the average tax rate is 30% anyway.

The new CGT regime applies to all assets, not just housing. The only exception being new builds of residential property where you have a choice of indexing and a minimum tax rate or the 50% discount. There is no pretty affordable housing bow on this one it is a pure tax grab from those in the lower tax brackets, that do not have other income to first bring them up to $45,000 where the 30% tax bracket kicks in. It is not the discount or indexing that is the problem it is the minimum tax rate of 30%. This means people without other income will be taxed on the same average tax rate as a person who earns $227,000 a year.

This is a clear punishment of the risk taking investors on a low income, paying more tax than those that have a less risky source of income such as interest, superannuation and wages. Add to this the restrictions on negative gearing and landlords are voting with their feet, clearance rates have dropped, who is going to provide rental properties for those that cannot afford to buy?

The latest attack on Mum and Dad investors is that self managed superannuation funds will no longer be able to borrow to buy residential properties. So even less landlords in the market. Which means less rental properties available leading to homelessness.

The very fact that auction clearance rates have dropped so far shows that first home owners cannot pick up the slack even when prices drop. The property market is being destroyed, people are losing equity, those that utilised the governments 5% deposit scheme now owe more to the bank then their house is worth. Nothing here deals with the real problem, not enough houses in the first place.

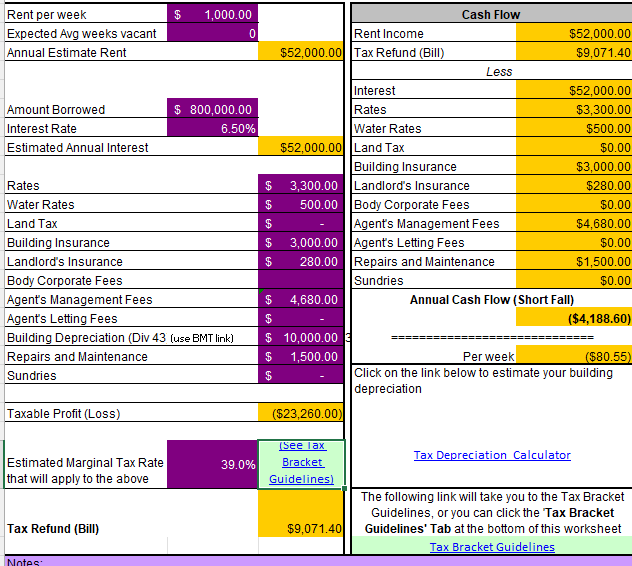

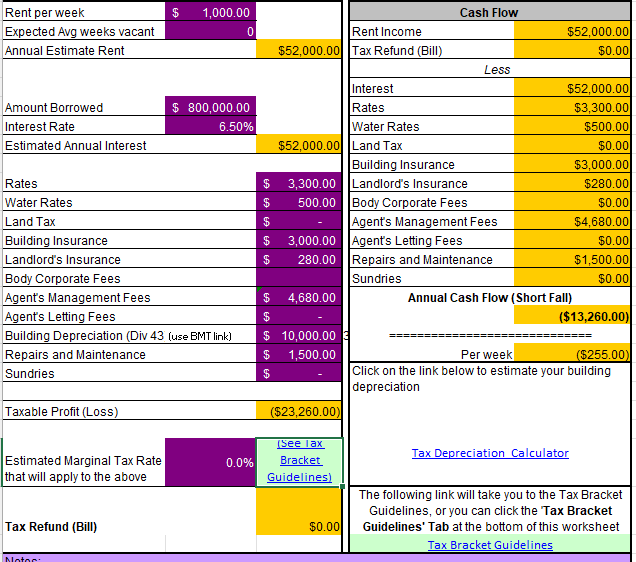

The negative gearing restrictions also hit the non wealthy the hardest. If you already have properties in your portfolio that have, over the years, finally become positively geared then you can buy a negatively geared property and deduct the losses against the income on your other rental properties. So, it is just the first time landlord wanting to own just one investment property that is hit by the restrictions on negative gearing. This is a complete reversal of the suggestion that maybe only people who have more than a couple of rental properties should have their tax concessions pegged back. I did some numbers on a basic property, see the bottom of this blog. If you can utilise the negatively geared advantage the sample property will cost $80 per week to hold. If you can’t because this is your first property this very same property will cost you $255 per week to hold. So now the wealthy with multiple properties can buy their next property cheaper in a depressed market and charge higher rents because there are now less landlords. This whole strategy is skewed to favour the wealthy, how did a Labor government get so misled!?

But wait there is more, hidden in the fine print, even the 50% CGT discount that is supposed to apply to gains up to 1-7-2027 is unlikely to eventuate. It has been attacked by the order of the CGT calculation. It is complicated to the point of being deceptive. Bear with me, this is taxation by stealth that needs to be exposed. Further, the cost to calculate your capital gain is going to increase exponentially. The complications designed to hide the tax grab are difficult to understand and best explained by example.

So, you are about to retire and need to sell off some assets you have held outside of super. Fortunately, you didn’t try and protect those assets by holding them in a discretionary trust, it could have been even more complicated. You found it necessary to keep some of your savings outside of super just in case you needed the money (possible medical expenses or roof repairs) before you reach preservation age. Unfortunately, the next generation is not going to have that option they will be punished too heavily for saving outside of superannuation but what do they do if they need money before they are 60?

Here are the assets you decided to sell, there is a house purchased before 1st July 2027 and a parcel of shares inherited before 1st July 2027. After 1-7-2027 you invested in a listed company and participated in their dividend reinvestment scheme. This means that twice a year instead of receiving cash for your dividend you purchased more shares. You still had to pay tax on the dividend of course. You also have some carried forward losses because the year before some shares you owned in a poorly performing company were compulsorily acquired, bought back for less than you paid for them giving you a $1,000 carried forward loss.

The parcel of shares you inherited in 2000 were pre CGT assets to your parents so your cost base is market value in 2000 which was $5,000, they were worth $7,000 at 1-7-2027, now worth $10,000. Due to indexing the cost base is $7,700 so a post 2027 gain of $2,300 No DRP just one full parcel. The house purchased in June 2026 had a capital gain of $10,000 before 1-7-2027 as the capital growth barely covered the stamp duty cost to buy. The house gained $20,000 post 2027 but selling costs were $30,000 so there is a post 2027 loss of $10,000 so no indexing of the cost base.

Indexation applies individually to each dividend reinvestment. If there is a loss it cannot be increased by indexation, the game is rigged, the government is only on the bandwagon when you are winning. If indexation is more than the gain then the gain is considered to be zero. So the DRP shares would be treated as follows:

| Indexation Rate | Indexed Cost Base | Selling Price | Gain(loss) | |||

|---|---|---|---|---|---|---|

| Shares first parcel 1-7-2027 | $200,000 | 2,000 shares at $100 each | 10% | 220,000 | 230,000 | 10,000 |

| DRP 30-10-2027 | 5,000 | 50 shares at $100 each | 9% | 5,450 | 5,750 | 300 |

| DRP 30-3-2028 | 5,100 | 45 shares at $114 each | 9% | 5,559 | 5,175 | 0 |

| DRP 30-10-2028 | 5,200 | 45 shares at $115 each | 8% | 5,616 | 5,175 | (25) |

| DRP 30-3-2029 | 5,300 | 44 shares at $120 each | 0% | 5,300 | 5,060 | (240) |

| DRP 30-10-2029 | 5,000 | 42 share at $118 each | 0% | 5,000 | 4,830 | (170) |

| Cost | $225,600 | 2,226 shares | ||||

| Sell 31-12-2029 | $255,990 | 2,226 shares at $115 each |

Now this is how it gets complicated. Any losses have to be first offset against the pre 2027 capital gains on the shares then if any losses still remain they are offset against the pre 2027 gains on the house. In other words post 1-7-2027 losses are offset against gains entitled to the 50% CGT discount before the discount can be applied, possibly leaving nothing to be discounted. Then if any gains remain they must be offset against the $1,000 capital loss carried forward from last year. Further, consider that the residential investment property that you are selling was purchased just after 12th May 2026, in ignorance of the budget ramifications, now you realise that you cannot afford to carry it into retirement, it has been sold. During the ownership period this property has made a loss on the rent of $15,000 that has been quarantined and can only be offset against positively geared residential rents or capital gains on residential properties, not against the capital gains on the shares.

Each segment of the CGT calculation:

| Carried forward losses from previous years compulsory acquisition of shares | $ 1,000 |

| Inherited shares pre 1-7-2027 gain | $ 2,000 |

| Inherited shares post 1-7-2027 gain | $ 2,300 |

| House pre 1-7-2027 gain | $ 10,000 |

| House post 1-7-2027 loss | $ 10,000 |

| DRP Shares post 1-7-2027 gain | $ 10,300 |

| DRP Shares post 1-7-2027 loss | $434 |

So from the figures above this is how the losses are offset, current year losses before carried forward losses. Offset against pre 2027 non residential capital gains then offset against pre 2027 residential capital gains, then against post 2027 non residential capital gains then offset against post 2027 residential capital gains, as follows:

| Pre 2027 CGT capital gain on inherited shares | $2,000 |

| Reduced by post 2027 loss on DRP $25+240+170= | $434 |

| Less loss post 2027 on house $10,000 but only use | $1,566 |

| Pre 2027 gain on inherited shares eliminated by post 2027 losses | |

| Pre 2027 gain on house | $10,000 |

| Less balance of post 2027 loss on house | $8,434 |

| $1,566 | |

| Reduce by the loss carried forward from last year | $1,000 |

| This is all we have left of the pre 2027 gains | $ 566 |

Fortunately, it is still a residential capital gain so we can offset some of the $15,000 in quarantined negatively geared losses on the rental property but not much of them, only $566. The rest are never likely to be realised and could not even be used to create a capital loss to offset against other capital gains.

The above brings us back to zero, the remaining capital gains are:

| Inherited shares post 2027 capital gain | $ 2,300 |

| DRP shares post 2027 capital gain | $10,300 |

| $12,600 |

Taxable at a minimum of 30% because the pre 2027 gains have been eradicated by the post 2027 losses and the quarantined negative gearing losses can only be offset against residential rental property capital gains or other positive geared rental property income. Note a better tax outcome might have been achieved on the house if the net gain was averaged over the whole period of ownership so your Accountant will need to go back over the figures and the loss offsetting again to compare. $$chingching$$

Now let’s look at how much tax a taxpayer would pay on this $12,600 depending on their other income:

| Tax Payable | |

|---|---|

| Not yet 67 living off savings earning $20,000 a year | $3,780 |

| Student full time study part time work earning $20,000pa | $3,780 |

| Carer only working part time earning $45,000 | $3,780 |

| Age Pensioner receiving $31,000 in pension plus a tax free Superannuation income stream on $320,000 around | $2,500 |

| Age Pensioner receiving $140 in pension plus a tax free Superannuation income stream on $720,000 | $0 |

| Wage earner earning $120,000 a year | $3,780 |

| Self Supporting Retiree an income stream on $10mil in super | $3,780 |

| Wage earner earning $500,000 a year | $5,922 |

Apparently this is fairer!!!! Looks to me like it sucks to be trying to live off your meagre savings or studying.

Another way of explaining the minimum tax rate is that a taxpayer with no other income than that which is subject to the minimum tax rate ie discretionary trust income and capital gains, is not entitled to earn their first $18,200 tax free, considered to cover the bare minimum cost of survival. They are also not entitled to only be taxed at 15% between $18,200 and $45,000. With a minimum tax rate of 30% applied to this low income that is an extra $9,480 in tax paid by someone on a very low income. That is nearly $200 per week, the grocery bill now gone in tax. The carve out for low income earners in our tax rates, was intended to ensure people only paid tax when they could afford to. On the other end of the scale a person with income of $227,000 has an average tax rate of 30% anyway so the minimum tax rate makes no difference to the amount of tax they pay. Same for all income above that amount too. Make no mistake this minimum tax rate is a tax on the poor, it makes no difference to the wealthy.

Be careful here making a donation or putting money into super is unlikely to reduce the tax payable on your capital gain as the 30% is a minimum no matter how much you reduce your taxable income. No matter what, unless you are getting an income tested Centrelink payment, the minimum tax on this $12,600 is $3,780. Superannuation contributions or donations are only going to help your tax position if your income is more than $45,000 plus the capital gain.

A far fairer way would be to at the very least put the superannuation income stream into the tax return to determine what tax rate applies or better still start taxing super like any other form of income. We have a perfectly good tax system based on ability to pay that steps up the tax bracket as income increases. All this fiddling is a smoke screen to shift more of the tax burden onto the poor. The wealthy and the superannuation funds have conned the government in my opinion.

Further, capital gains are made over many years. The argument for a 30% minimum tax rate was to avoid people delaying selling investments until they retire and are in a lower tax bracket. It is quite possible they are only in that lower tax bracket because they have all their wealth tied up in a tax free superannuation pension. So, they wouldn’t be in that lower tax bracket if their superannuation income stream was taxed!

The position in Keating’s day was to divide the gain by 5 and apply that tax rate to the remaining 4/5ths because it is not fair to tax investors on a gain made over many years all in one year pushing them into a higher tax bracket. Granted that in Keating’s day you didn’t have retirees living on all this tax free superannuation income but this is not the way to fix the problem as it has too many inequitable consequences. The solution is to tax those superannuation income streams and leave the low income battlers alone. No, superannuants are not saving the country money. Once they have more than $1.6mil in superannuation the tax they save on the earnings being tax free is more than the full age pension. They are not self supporting at all they are costing us more than age pensioners.

Please help to get this word out there, push back against the propaganda. I give permission for this blog to be published by anyone, just please don’t change it.

Julia Hartman B.Bus CA FTI

Registered Tax Agent 75181003