Julia's Blog

Julia's Blog

The most important message is there is nothing in the proposed legislation that suggests you should off load your existing residential rental property.

Negative Gearing

Residential properties purchased after 12th May, 2026 will not be able to offset their rental losses against other income such as wages after 1st July, 2027, unless it is a new build.

This means you should think twice about selling a property you already own, for two reasons. Firstly, that there are fewer buyers in the market now, for established properties, so prices are likely to have dropped. Secondly, the property you now hold can continue to be negatively geared so more beneficial than an established property you might buy in the future. Not to mention the buying and selling costs.

Note that if you have properties in your portfolio that are positively geared you can offset losses from a residential property purchased after 12th May, 2026 against the positive rental income. Maybe all the more reason to keep your pre 12th May, 2026 property as you can negatively gear it now and when it does become positive you can purchase another established property, maybe at a bargain price and offset the losses.

This is just one of the many ways this budget misses its mark. Well established property investors can continue to negative gear because they will have some positively geared properties to absorb the loss. It is only punishing new first time landlords.

In fact, having a positive for tax purposes residential rental property portfolio may put you in the perfect position to snap up a bargain now because you can absorb those losses. Note if you are thinking of snapping up a bargain anyway the loss that you can’t offset can be saved up and used when the property becomes profitable or you make a residential capital gain.

It should be noted that commercial property and shares can still be negatively geared. Further, if you purchased your home before 12th May, 2026 and it later becomes a rental it will be entitled to be negatively geared.

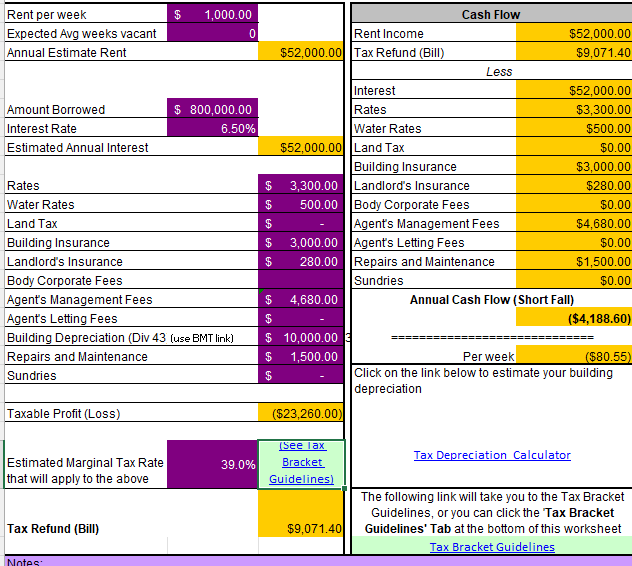

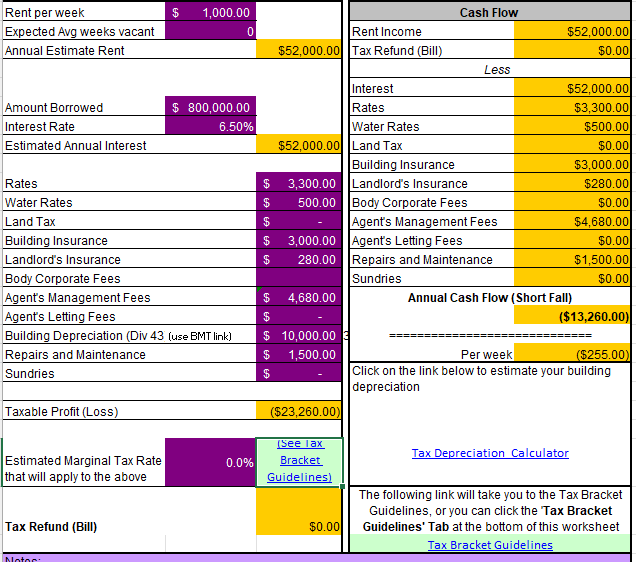

The following two screenshots show what the removal of negative gearing on residential properties has done to the cost of holding a rental property. This property purchased before the budget would cost you $80.55 a week to hold. If purchased after 12th May, 2026 it will cost you $255 per week to hold. If you would like to do some what ifs with your own figures the calculator is available here https://www.bantacs.com.au/shop-2/property-cash-flow-calculator/

Pre Budget

Established Residential Property Purchased after Budget

New Builds

Newly built residential properties are in a unique position, they can be negatively geared and entitled to the 50% CGT discount without the 30% minimum CGT tax rate. It is expected that demand for new builds will increase, pushing prices up. Be careful to budget for the lead time on construction. Also consider new builds are less likely to be located in well established areas.

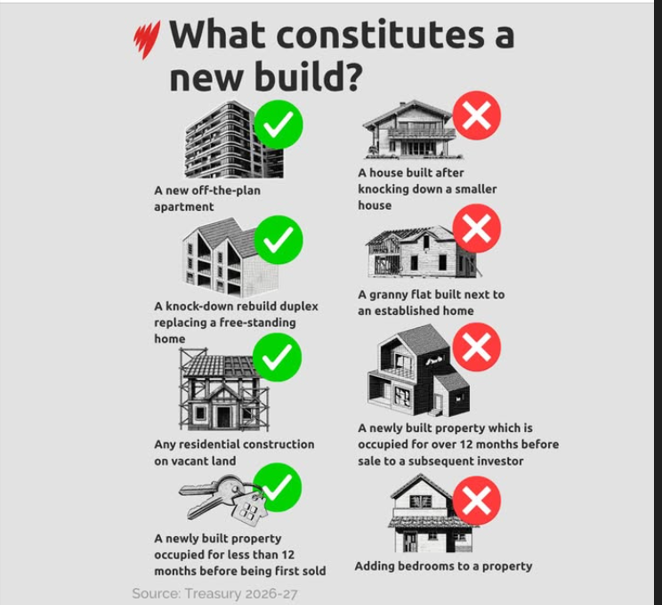

What constitutes a new build has not yet been legally defined. The following summary is from the Treasury website.

Possibly there is a market opportunity in buying and established home in an established area in the currently depressed market, knocking it down and building a duplex thus qualifying as a new build. Of course there is a lot to consider in such a project. For the tax considerations read https://www.bantacs.com.au/Jblog/knockdown-and-rebuild-your-home-or-a-duplex-tips-and-traps/#more-2007

How the Capital Gains Tax will work

For all investments other than new residential properties, any capital gains made over and above the market value as at 1st July, 2027 or after purchase date if purchased after 1st July, 2027, will be taxed at a minimum tax rate of 30%. The gain will be calculated after allowing for indexing of the cost base for inflation but there will be no 50% CGT discount. Note the 30% minimum tax rate will not apply to recipients of an income tested Centrelink payment and capital gains do not affect age pension entitlement.

The government’s intent is to discourage people from waiting until they retire and are only receiving tax free superannuation income before they sell the property thus making the most of the lower income tax brackets. But let’s look at just how much the minimum 30% tax will cost if you have no other income. Afterall once income reaches $45,000 it is in the 30% tax bracket anyway.

$45,000 x 30% = $13,500

$45,000 – $18,200 = $26,800 x 15% = $4,020

Difference is $9,480 extra tax due to the 30% minimum tax rate but if it is a big gain giving you a total taxable income of $227,000 then your average tax rate will be 30% anyway so no difference in tax payable whether the minimum tax rate applied or not. Though of course the 50% CGT discount not applying may make a huge difference, depending on the CPI.

The crazy thing about this supposed budget for the workers is that the minimum 30% tax rate is only going to hurt those on a low income. If they really wanted to even up the tax playing field they would be taxing superannuation income streams over $80,000 as it is at $80,000 that the tax savings on superannuation exceed the cost of the single age pension and taxpayers are subsidising wealthy superannuants more than age pensioners.

What Now for Property Investors?

Not going to predict the future here other than to suggest you consider the following points:

- After 2 years of no negative gearing in the 80s Paul Keating was forced to reverse his decision.

- The budget forecast itself states that the tax policy will reduce housing stock by 35,000 houses.

- Housing prices and rents are high because we have an extreme shortage of houses.

Don’t forget the basic fundamentals. Supply and demand and the value is in the land if there is a shortage of land supply. This suggests there is a better opportunity for capital growth in established areas.

The intention of this budget is to move housing away from rentals towards owner occupiers. Reducing the supply of rental properties will increase rents and of course increase homelessness!

Now considering the budget changes and the cashflow example above it is going to be a lot harder to afford to hold an established rental property. For this reason it is probable that prices of established properties will drop, helping affordability a little and with less new landlords joining the market rents will increase.

If you are thinking of buying a new build just remember it will be an established property when you decide to sell so you are going from a high demand market when you buy into a lower demand market when you sell. Further, it may be difficult to find a new build in an established area where the supply of land remains the same yet the demand for housing increases. Maybe the perfect fit is buying an old residential or commercial property with the idea of one day building a duplex thus qualifying for the new build concessions. It will be interesting to see how this pans out. It maybe that you could accumulate large capital gains on the value of the land in an established property then build a duplex and qualify for the 50% discount when you sell.

It seems to be accepted and already starting to show that prices of established homes are dropping. Maybe there are some bargains to be had, maybe the drop has a lot further to go? What is your risk rating and ability to cope with a negative equity situation if you buy too soon? Watch auction clearance rates each week.

The Warren Buffet philosophy, buy while others are fleeing the market, is manageable in a share market where you can just sell off what you need quickly if you need funds to make loan repayments etc but with property you may have to sell the whole house if you get caught short rather than ride out the negative equity. Tread carefully making sure you are not forced to sell. A long-term hold will make any initial hiccup in buying price insignificant. Times have changed dramatically make sure you fully understand and are not just following what has worked for you in the past. To help you prepare use the free Moorr platform https://empowerwealth.com.au/access-to-our-money-portal/