Julia's Blog

Julia's Blog

I am very disappointed with this budget it claims to help people buy their own home but throws the homeless and those not in a position to buy under a bus.

A small investor buying an established home to provide rental accommodation will pay more tax than an investor in shares, commercial properties and new homes. It might have a red bow on it but it is a specific attack on people who provide residential accommodation to those that cannot afford to buy their own home. Right now, as at budget night, the worse possible investment option for mum and dad investors is an established rental property so new rental listings will dry up overnight!

The budget documents themselves admit it will reduce rental supply and increase rents! Yet they are selling it as a solution to the housing crisis. It is really just a tax grab from one specific section of the economy, those providing accommodation to the poor.

Key Points

- From 1st July 2027 losses from residential rental properties purchased after 7.30pm on 12th May, 2026 can only be offset against profits or capital gains from residential property unless the loss is from a new build.

- Capital gains made on all assets after 1st July 2027 will not receive the 50% CGT discount unless the asset is a new build residential property. There will be indexing for inflation and a minimum tax rate of 30%

- Assets purchased before 20th September 1985 are to lose their CGT exemption on gains made after 1st July, 2027.

- From 1st July 2028 trustees of discretionary trust will be required to withhold 30% tax from most distributions, this tax can be used as a non refundable tax credit by some beneficiaries.

- Bucket companies are likely to be double taxed so no longer a strategy

- Permanent allowance of an immediate write off for business buying plant and equipment costing less than $20,000

- Companies making a loss will be able to claw back tax paid on previous profits.

- Start up businesses will be able to offset their PAYG withholding bill and or FBT bill with business losses made in the same year.

- Workers and sole traders will receive a $250 tax offset starting in the 2027-2028 financial year.

- EV FBT concessions to remain until 1st April 2029

Tax Offset for Workers

WATO the Working Australians Tax Offset of $250, is an actual reduction in tax payable by all workers earning over $18,200 from 1st July, 2027 ie the 2027-2028 financial year. Only available to taxpayers who have income from wages, salaries or sole trader business income.

PAYG Instalments

This is where the ATO send you regular tax bills to pay next year’s tax by instalments because you have income that is not taxed at source. If you found these notices annoying and tended to ignore them, now is the time to start paying attention. If you have a history of non compliance they will put you onto monthly instalments and those notices will become a lot more annoying.

Capital Gains Tax

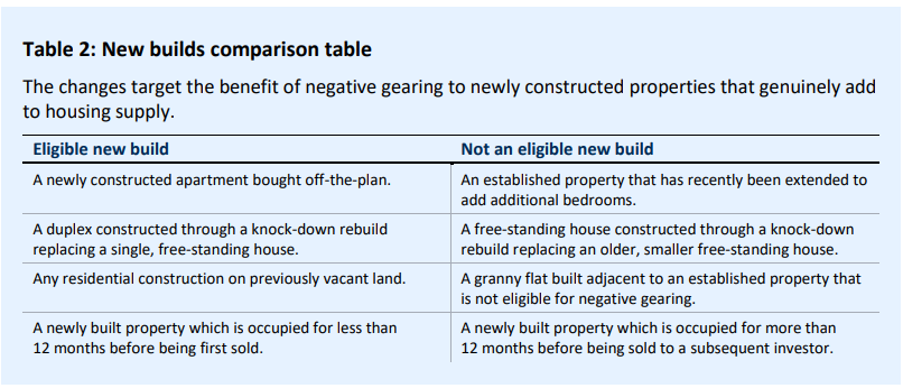

Note these changes will only apply to capital gains made after 1st July, 2027. As you are no doubt aware the CGT event is considered to have taken place when the contract of sale is signed, not settlement. The 50% CGT discount will be removed effectively from gains made on all assets, even pre CGT assets, after 1st July, 2027 unless the gains are on “new build” residential property acquired after 12th May, 2026. New builds are defined in the budget fact sheet as follows:

From 1st July, 2027 all assets other than new builds will have their cost base indexed for inflation and the gain subject to a minimum tax rate of 30% unless the owner is a means tested income support recipient. The cost base will not be entitled to indexation until the property has been owned for over 12 months. Note there is nothing to gain by rushing out and selling before 1st July, 2027. Though you might begin to question why you should continue to hold the property now that the capital gains will be taxed at such a high rate.

Negative Gearing

From the 1st July, 2027 a loss on a residential rental property that is purchased after 12th May 2026 will not be able to be offset against income from other sources, only against other residential rental properties making a profit or capital gains from a residential rental property. If no such offset is available in the current year then the losses can be carried forward indefinitely until utilised. That is unless the property is considered a new build acquired after 12th May, 2026. In that case losses can be offset against other income. For a residential rental property to be considered purchased after the 12th May 2026 the contract would probably need to be entered into after that date.

So if you have already signed an agreement to buy before 7.30pm on 12th May 2026 you will be entitled to negatively gear an established residential property or a new build. But if you sign after 12th May, 2026 you will only be entitled to negatively gear a rebuild.

Note it is only residential rental properties held by mum and dad investors that cannot be negatively geared, the big end of town can still negatively gear residential investments. Further, commercial properties, shares etc can still be negatively geared by all, yet this budget is promoted as helping with the housing crisis?!? Where is the assistance for renters? This policy will instantly stop investors buying established residential rental properties, well before and government plans to increase supply come into fruition. Without the continuing entry of new investors into the rental market there will be a sudden drop in supply, rents and homelessness will increase. Hopefully, just as happened in Keating’s day this policy will have to be very quickly dropped or the senate will see sense.

Practical application

Residential Property Owned Before 12th May, 2026 – Gains up until 1st July, 2027 will be entitled to the 50% CGT discount. Any gain from 1st July, 2027 will be calculated using indexation and the minimum tax rate of 30%. So how is the line in the sand is drawn? You can choose either

- Obtaining a valuation as at 1st July 2027 calculating the gain before that date using the 50% CGT discount and then using that valuation as the first element of the cost base going forward, indexing that for inflation with the difference between the indexed cost base and the selling price being the capital gain that is to be taxed at a minimum of 30%.

or

- The gain over the whole period of ownership is apportioned on number of days before 1st July 2027 and number of days after 1st July 2027 to determine the notional cost base at 1st July 2027. This is unlikely to produce the best outcome. But don’t rush valuers can provide historical valuations when you are ready to sell.

It is expected that the above will not be quite so simple when the cost base has been reset to market value on death or home first used to produce income. It is hoped that this will be fine tuned to simply make sure there is no ambiguity and the original intentions are maintained.

These pre 13th May 2026 properties will be able to have any losses offset against other income.

Residential Property Acquired After 12th May, 2026 But Before 1st July, 2027

Acquired means the contract was entered into after 12th May 2026. Unless this is a new residential property, after 30th June 2027 you are not going to be able to negatively gear the property other than to offset the loss against income from other residential rental properties or residential capital gains. If the losses cannot be offset they can be carried forward indefinitely.

When sold after 1st July, 2027 you will be subject to CGT with the 50% CGT discount on the gain up to 1st July, 2027. Any gain after that date will not be entitled to the 50% CGT discount, just indexing from 1st July, 2027. Further there will be a minimum tax rate of 30% on that gain.

Now this is where the choice between apportioning the capital gain and using the market value at 1st July, 2027 will likely be in favour of pro rata. You see the cost base up to 1st July, 2027 will include the stamp duty, improvements and legals you paid. If this goes back to market value they are not included and considering the governments attack on the property market the market value will not have increased enough to cover them. Effectively creating a capital loss in the period where the 50% CGT discount could have applied and increasing the capital gain when there is no discount and a minimum tax rate of 30%.

Residential Property Acquired After 1st July, 2027

Acquired means contract entered into after 1st July, 2027. Unless this is a new residential property the losses from the property can only be offset against profits on other residential rental properties or capital gains on residential rental properties. Otherwise, these losses can be carried forward until used up. Any capital gain will be subject to a minimum tax rate of 30% and based on the difference between the selling price and the cost base indexed for inflation.

Property Acquired Before 20th September, 1985

From 1st July, 2027 the wonderful exemption for pre CGT assets will be gone. You will start with a cost base of market value from that time. From then on all the capital gain will be exposed to tax, though you will get indexing for inflation increasing the market value as at 1st July 2027. Note indexation may not kick in till 1st July 2028. The 30% minimum tax rate will apply. There is also the option of using an averaging of the gain over the period of ownership method of setting the market value as at 1st July, 2027 but I would not recommend this at all, as the value of the gain before 2027 is very likely to be higher than the gain afterwards and you may well have trouble determining the original price you paid and other relevant cost base items. From 1st July 2027 it is time to start keeping cost base records on pre CGT assets.

Note the practical examples above only look at established residential properties. Commercial properties, new build residential and other assets such as shares can still be negatively geared but the loss of the 50% CGT discount applies to all assets other than new build residential rental property acquired after budget night. New builds have the option of using either the 50% CGT discount or indexation with a minimum tax rate of 30%.

Regarding valuations, valuers should be able to give you historical valuations in the future, there is no need to run out and try to find a valuer on 1st July, 2027.

Tax on Trust Distributions

Starting from 1st July, 2028 there will be a minimum tax rate on profits made in discretionary trusts of 30%. This is then passed onto the beneficiary as a non refundable tax credit they can use to offset the tax on the distribution they receive. Note if the beneficiary is a company they do not receive this tax credit. Further this tax paid by the trust on the company’s distribution is not credited to their franking account. As the tax credit paid by the trust is not refundable to even non corporate beneficiaries, if the trust distribution is their only income they get no tax free threshold hold or lower tax rate up to $45,000. They could receive $30,000 from the trust and have to pay $9,000 in tax so have to live on $21,000. Higher income beneficiaries would not be so badly affected as they can use other income to soak up their tax free threshold and 15% tax bracket then use the 30% withheld from the trust to cover the tax on the trust distribution. A fact sheet provided by Treasury implies that income subject to the minimum tax of 30% can be considered taxed at your personal highest tax rate, no need to average etc. So a the 30% non refundable credit can even be used to pay the tax on wages and get a refund of the tax paid by the employer. The unfair treatment is for low income earners. The low income beneficiary is in the same tax rate for all of their income as a person earning $135,000 a year pays on the higher portion of their income.

Yes, transferring investments out of trust is well worth considering but you need to weigh up stamp duty and CGT consequences. The government intends to introduce attractive roll over measures and hopes to get the states on board regarding stamp duty and the like.

Don’t let this put you off distributing trust profits. If you leave the profits in the trust it will be taxed at the maximum tax rate of 47%. This is another reason to consider rolling into a company, though a treasury fact sheet implies that a company may not get indexing on its capital gain. A lot depends on just what you hold in the trust.

Any franking credits held by the trust must be used to pay its 30% tax. It is possible that there could be more franking credits than the 30% tax. Nothing said so far as to whether there will be any change to the distribution of franking credits. No change would mean that the remaining franking credits could be distributed to beneficiaries who may be able to have them refunded if they can pass the 45 day rule.

The budget makes it clear the goal is to persuade people to move from discretionary trusts to fixed trusts or companies and provides rollover support to achieve this. Which is only possible if you control the trust but that is the whole point of discretionary trusts it is the trustee that has control not the beneficiaries. These are commonly used to provide for people unable to provide for themselves.

If you are operating a business then you would be better off running through a company where you may well qualify for the 25% tax rate. But be careful about holding investments in a company as the treasury fact sheet implies that companies will not be entitled to indexation.

There is a carve out for primary producers, income of vulnerable minors, non residents but only for testamentary trust existing at 12th May, 2026. So if you are thinking of trying to provide for your disabled child or your spouse by setting up modest investments in a trust for them you need to consider their tax rate is going to be as high as someone who earns $135,000 a year and maybe you better put it in their name. If you don’t think they have capacity to deal with this you are caught between that risk and tax penalties because of this policy. Time to revisit your will.

Bucket companies will probably be double taxed. The trustee withholds 30% of their distribution entitlement. The bucket company will not be entitled to a credit for that 30% tax withheld yet it will be taxed again on the 70% it receives. Further, they may not get indexation on any future capital gains on investing the money.

Small Business

Finally, certainty with the immediate write off deduction. Spend $20,000 or less on an asset for your business and it can be claimed as an outright tax deduction. This is now permanent.

From the 2026-2027 financial year, companies with turnover under $1 billion will be able to carry losses back, up to two years, to offset previous company tax paid. In other words receive a refund, providing the tax has not been distributed as a franking credit.

From the 2027-2028 financial year, start‑up companies with turnover under $10 million will be able to access a refundable tax offsets for losses incurred in their first two years. This offset can be used to cover or claw back PAYG withholding payments and FBT liabilities that apply to the loss year.

Existing FBT concessions will continue for electric vehicles until 1st April 2029 after that date ie the 2029-2030 FBT year the concession will be reduced to a 25% discount but only in relation to new agreements.

My Two Bobs Worth

Any punishment dished out to landlords is going to reduce the amount of rental properties available. Not all renters can afford to buy a home, no matter how low the cost. The budget papers admit that the measures will reduce rental stock by 35,000 houses but claim their other measures will make up for this. I fear there will be a huge timing difference!

Meanwhile huge amounts of superannuation income remain untaxed. For example a person can hold the investment property in their SMSF and sell when they are in pension phase so pay no capital gains tax at all.

Anyone considering buying an established property to hold as a rental is unlikely to be able to afford to hold it without being able to offset the losses against other income, such is the disparity between the cost of properties and rent received. The government are trying to encourage future investors to build new properties and increase housing stock. But consider that the 2019 introduction of no deduction for interest on the loan for the land while building a rental property means it would be a very wealthy person indeed who could afford to build new.

Most mum and dad investors have now been kicked out of the market going forward. Other than buying in a SMSF where borrowing is more expensive, it is unlikely that established residential rental properties will stack up as an investment. As stated in the budget papers these investments make a loss for up to 10 years, why would anyone subsidise housing to that extent? Further, buyers of established rental properties are not going to be able to pull money out of thin air if the tenants destroy the place. Yet if they have several residential properties they will be able to offset the loss against profitable properties or capital gains on residential property, so the really wealthy will not be hurt by this measure. Nor are the big institutions who receive a carve out.

Keating tried this back in the eighties and very quickly had to reverse the decision to avoid a housing crisis.

Very disappointed that a Labor government is introducing measures that set a minimum tax rate on many individuals of 30% when, in many cases, the company tax rate is as low as 25%. We have a perfectly good step up tax rate system that determines tax liability on the ability to pay. Now we are going to have people receiving investment income from a trust losing nearly a third of it when previously the income might not have even been enough to have to pay tax on! Yet still the assets in the trust may be deemed so high that they don’t even qualify for the pension. These are generally people who do not have the option to work due to disability or age and are not in a position to change how the investments are held either because of CGT and stamp duty or that they do not control the trust because someone who cared about them set it up for their benefit.

The budget papers have the hide to say that they are allowing rental losses to be carried forward so that landlords are not discouraged from undertaking repairs. But the government offers no advice on how landlords will be able to afford these repairs if they have to pay tax on money they don’t have because they have an expense relating to a source of income that they cannot offset. Consider a bad tenant that stops paying rent and damages the property, repairs, rates and insurance alone are going to put that property into a loss let alone the interest expense. Where does the money come from?

The budget claims to enable 75,000 Australians to buy their own home over the next 10 years. Firstly, the population is increasing by more than twice that number, every year. The budget claims to produce 30,000 new public housing homes over the next 10 years. There is nothing in this budget to help renters and the homeless, right now! Those who are never going to be in a position to own their own home, it just punishes their landlords. Grandfathering might protect some but with these huge disincentives to new landlords, natural attrition will either see rents rise or housing supply decrease when the biggest problem, all agree, is the lack of housing supply.

To quote the budget papers:

“Lower house price growth will have a modest impact on housing supply, with the increase in supply over the next decade expected to be only around 35,000 dwellings fewer compared to no tax policy change”

Apparently, that is acceptable because they are putting infrastructure in place that will support up to 65,000 homes, not sure who is going to build them and when they will be any help to renters and homeless.

What Now?

As long as you signed the contract before 7.30pm 12th May, 2026 you are still entitled to negative gear so the affordability decision remains the same. It is the true benefit of the overall investment strategy that needs to be reconsidered as you will miss out on the CGT concessions you were anticipating. Nevertheless, you are on the hook, incurred an incredible amount of expenses and state taxes to get into this investment. No point in incurring more expenses to get out.

Your tax refund is safe for your currently property portfolio. If you now buy an established residential property your 2027 refund is safe but after that you will only be able to offset losses on the property purchased after 12th May, 2026 against profitable residential properties or residential capital gains unless the property you purchased was a new build. This is going to significantly affect your cash flow. This spreadsheet will help you work out how much. https://www.bantacs.com.au/shop-2/property-cash-flow-calculator/ Simply remove the tax refund amount from the right hand side

If you are still toying with the idea of buying a rental property you may be tempted to buy brand new. If you are thinking of buying the land and building, consider the cost of not being able to claim the interest on the land during construction and not receiving rent for that period. Consider you are betting on capital growth in a market the government is trying to cool down. If you are thinking of buying an established property the numbers are unlikely to stack up as well as they did before 12th May, 2026. In all likelihood, if you are a small investor you will not be able to afford the property without the benefit of being able to offset the expenses exceeding the rent, against your wages income.

Consider a SMSF which will be able to offset the losses against other income it receives such as superannuation contributions you make and claim a tax deduction for. Effectively, getting a deduction for the loss on the investment property in your tax return by contributing enough to the super fund to cover the property loss. Note there are cap limitations on contributions, SMSFS are expensive to run and a higher interest rate on loans.

You may now only be able to afford a residential property if you can increase the rent. With other residential investors being in the same boat as you that is a possibility, let’s wait and see. The budget forecast admits rents will increase but claim the increase will only be $2 per week. Even if you believe that, the question remains how is this helping renters, reducing supply and increasing rents.

Regarding the minimum tax rate of 30% on capital gains made after 1st July 2027, there is still an advantage in holding till retirement if you can manage to qualify for at least a small age pension. You see capital gains are not included in income for pension purposes. Obviously, the value of the asset will be deemed but if you just get that, much sort after, $1 in pension you will be considered an income support recipient so not subjected to the minimum tax rate of 30% on capital gains.

Regarding the 30% minimum tax rate on trust distributions. While not completely clear it appears the you can consider the trust distribution to be taxed at your highest marginal tax rate, the 30% non refundable credit can be used to pay tax on your other income. If your only income is from a trust it is better to take wages of at least $45,000 to bring yourself up into the 30% tax bracket for any profit distribution you may receive. This is not going to be possible if the trust income is passive income. Careful here the trust is not going to get a tax deduction for those wages if it does not relate to the earning of income ie relate to trust business not passive income. Get this wrong and you could have a double tax situation where the wages are taxable to you but not deductible to the trust so the profit remains the same and has to be distributed out to you.

If you do end up buying an established residential investment property don’t just automatically think best in the high income earners name, now that there is no negative gearing. Or for that matter now it maybe best in the low income earners name for a lower tax rate when it eventually becomes positive, who knows what your circumstances will be then. Get out your crystal ball! Add to the possibilities that if you keep the property for decades the capital gain maybe in the hundreds of thousands ie higher than the minimum 30% tax rate but if the capital gain is split over two retired owners it may end up being less than $135,000 each so some tax to be saved at this end because of two tax free thresholds and the step up rates.

If you have losses in one discretionary trust where you have been distributing profits from another discretionary trust to offset, this will probably not work after 30th June 2028. From the 2028-2029 financial year that profit distribution will come with a non refundable tax credit for the 30% tax paid by the profitable trust. When this goes into the loss trust it is wasted. So the profits moved across will be taxed at 30%. You need to work on ways to get as much profits into this loss trust as quickly as possible to use the losses up. Completely different approach, you need to delay deductions.

Unclear or Unanswered Questions – We Will Keep You Posted

- Are bucket companies going to be double taxed on trust distributions? The non refundable tax credits paid by trusts do not flow to company beneficiaries. This means the trustee pays tax on the company’s distribution at 30%, and the company is then taxed on the net distribution ie 70% without access to those credits. An effective tax rate of 51% (but at least with 21% in franking credits) something that will make trusts drop bucket companies like hot potatoes from 1st July 2028.

- How indexation and the market value line in the sand at 1st July 2027 will apply to the small business concessions where there is still some taxable capital gain. Especially when it would be so difficult to value a business as at 1st July 2027. What records do we need to keep?

- Do companies get indexation on their capital gains after 1st July 2027. They did back when CGT first came out and there was indexation but a treasury fact sheet only mentions trust, individuals and partnerships. Further, what if the company qualifies for the 25% tax rate is this going to be amended to tax capital gains at 30%. If so that full 30% will go into the franking account so at what rate can the dividend be franked? This could potentially reduce the eventual tax rate on the capital gain if dividends from capital gains are not traced all the way though.

- A trust must use its franking credits to pay the 30% tax on profits but it is possible that there will be franking credits left over. Are these still distributable to beneficiaries and if not needed to pay beneficiaries tax after using the 30% non refundable tax credit, can the franking credit be refunded. Assuming can use up the non refundable tax credit first to pay any income tax in the hands of the beneficiary.

- How does the non refundable tax credit work in with the 45 day rule? Will the trustee be able to use the franking credits to pay the 30% tax on distributions because after all the discretionary trust will have held the shares for more than 45 days. Then these franking credits are transformed into an non refundable tax credit that the beneficiary, who does not pass the 45 day rule can at least use to pay their tax. A vast improvement for beneficiaries of testamentary trusts with some limited discretionary power and where the trustee (normally a professional organisation) refuses to make a family trust election. Is there a risk that the non refundable tax credit received from the trust will be included as a franking credit for the purposes of the de minimis rule where even though you don’t pass the 45 day rule, because your total franking credits for the year are less than $5,000 you are entitled to use them.

- How is this going to pan out for testamentary trusts that come into existence after 12th May, 2026? So children won’t get taxed as an adult, they will cop 30%? There must be more detail to come on this.

- If move out of current PPR and turn it into a rental, as it was purchased before 12th May, 2026 will it be able to be negatively geared?

- Company structure – is the CGT going to be at 30% and the overall tax rate at 25%

There is a long way to go between the announcement and the legislation. I predict lots of issues will arise that have not yet been considered. Then the Senate should ask some pertinent questions such as how does (to quote figures in the budget papers) reducing housing stock by 35,000 homes and increasing rents help the housing crisis for those that cannot afford to buy their own home?

It would be a brave person who invests before this mess is sorted out. Possibly buy a vintage car, they are not subject to CGT!

To people wondering what structure to use for investment or to start a business get out the crystal ball. As the law currently stands companies have a CGT disadvantage because there is no 50% CGT discount so unlikely to be the best choice for investment or a business that will one day trigger CGT, if these changes don’t go through as planned. Even slight changes in the budget plans could affect who should be the shareholders of the company. It is not clear but companies may not qualify for indexation so still not a good option for CGT if the changes go through. Trusts are threatened with a far worse tax situation in the future than companies but there are issues that have not been addressed and probably a year’s wait until the legislation is finalised. Sole traders and partnerships do not provide the asset protection of a separate legal entity. Superannuation funds are the only entities left unscathed but even a self managed superannuation fund cannot run a business so only good for investment.

The best advice is to not do anything for the next year or so. So much for the productivity the government wants, we need to grind to a halt and wait and see.